Like the 3,200 other pages of evidence uncovered and descriptions of crimes on this site, this web page is only one part of a massive multi-state entanglement of government corruption and cover-up. See size

Evidence was uncovered in parts over years, and not in the same order as the crimes occurred or the evidence was created. Statements were made based on what was known at the time.

Dates are approximate because government filings and reports vary in some cases up to months if not This is part of cover up. One example is Oklahoma's Openbooks, which started out late with only a fraction of what was required to be added each year. Plus, the data was littered with data entry and spelling errors, meaning you have to go through one entry at a time. This amount to more than 17,000 entries in 2017.

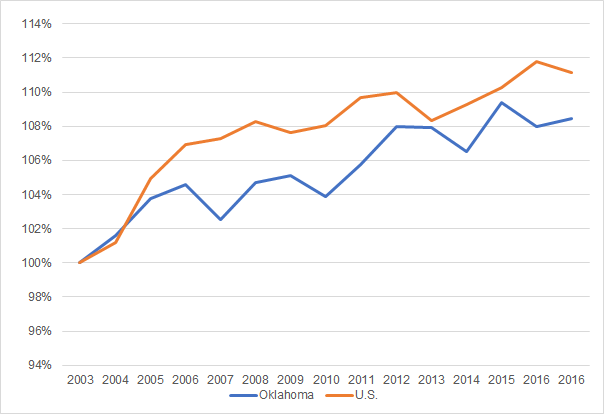

Oklahoma actual jobs v minimum and maximum jobs claimed to have been created to justify one of Oklahoma's 63 different undocumented tax credit types, Oklahoma Investment/New Jobs Tax Credits 68 § 2357.4.

Oklahoma Investment/New Jobs Credit 68 § 2357.4 allows tax credits equal to 1% of the amount invested or $500 per new employee for investments less than $40 million, or 2% of the amount invested or $1,000 per new employee for investments of more than $40 million.

- This is one of Oklahoma's oldest tax credits and is no information other than the amount of tax credits taken and cost to the public.

- The smallest in terms percent of investment allowed for tax credits, yet the largest total tax credits reported to have been allowed.

- We have other tax credits 68 § 2357.62 and 68 § 2357.73 reported as 68 § 2357.4 tax credits.